What is a Medicare Supplement (Medigap)?

Original Medicare (Parts A & B) covers most of your healthcare costs—but not all. You're responsible for deductibles, copays, and coinsurance that can add up to thousands per year. There's also no out-of-pocket maximum with Original Medicare, meaning your costs could be unlimited.

Medicare Supplement insurance (also called Medigap) is private insurance specifically designed to fill these gaps. When Medicare pays its share, your Medicare Supplement plan pays most or all of what's left—giving you predictable, low out-of-pocket costs.

How Medicare Supplement Works

- 1. You go to any doctor that accepts Medicare (no networks!)

- 2. Medicare pays its share of approved costs

- 3. Your Medigap policy pays most or all of the rest

- 4. You pay little or nothing out-of-pocket

Official 2026 Medicare Supplement Guide

Download the official government guide "Choosing a Medigap Policy" from Medicare.gov. This comprehensive resource covers Medicare Supplement basics, your rights, standardized plans, and steps to buying a policy.

Download Free Medicare Supplement Guide (PDF)Standardized Plans: A Through N

Medicare Supplement plans are standardized by the Federal Government. Each plan letter (A, B, C, D, F, G, K, L, M, N) offers the same benefits no matter which insurance company you buy from. The ONLY differences between are:

- Customer service

- Financial stability

- Premium stability

- Premium increase history

Important: Plan F and Plan C are No Longer Available for people have turned 65 after January 1, 2020

If you became eligible for Medicare on or after January 1, 2020, you cannot purchase Plan F or Plan C. These plans covered the Part B deductible, which is no longer allowed for new enrollees. Plan G is now the most comprehensive option available.

Comparing Medicare Supplement Plans

Here are the most popular Medigap plans and what they cover:

Most Popular Choice

Plan G covers everything EXCEPT the Part B deductible ($283 in 2026). Once you meet that deductible, Plan G covers 100% of your Medicare-approved costs for the rest of the year.

What Plan G Covers:

- ✓ Part A deductible ($1,736)

- ✓ Part A copays/coinsurance

- ✓ Part B copays/coinsurance (after deductible)

- ✓ Part B excess charges

- ✓ First 3 pints of blood

- ✓ Skilled nursing coinsurance

- ✓ Foreign travel emergency (80%)

What You Pay:

- • Monthly premium ($150-250 typical)

- • Part B Annual deductible ($283/year)

- • Part D Prescription Drug Plan

Lower Premium Option

Plan N has lower premiums than Plan G but requires small copays: up to $20 for doctor visits and up to $50 for ER visits (waived if admitted). Good for people who don't go to the doctor frequently.

What Plan N Covers:

- ✓ Part A deductible ($1,736)

- ✓ Part A copays/coinsurance

- ✓ Part B coinsurance (with copays)

- ✓ First 3 pints of blood

- ✓ Skilled nursing coinsurance

- ✓ Foreign travel emergency (80%)

- ✗ Does NOT cover Part B excess charges

What You Pay:

- • Monthly premium ($120-180 typical)

- • Part B premium ($202.90 in 2026)

- • Part B deductible ($283 in 2026)

- • Up to $20 copay per office visit

- • $50 copay per ER visit

- • Part D Prescription Drug Plan

Lowest Premium, High Deductible

High-Deductible Plan G has very low premiums but requires you to pay the annual ($2,950 in 2026) before the plan pays benefits. After that, it covers 100%. Best for very healthy people who rarely need care. Contact us to see how to get Plan G at a 30% discount.

How It Works:

- • Pay ALL costs until you reach $2,950

- • Same benefits as regular Plan G after deductible

Protect yourself from the $2,950 Deductible in the High-Deductible Plan G

What You Pay:

- • Monthly premium ($40-70 typical)

- • All costs up to $2,950 deductible

- • After deductible

- • Part D Prescription Drug Plan

Detailed Plan Comparison Chart

Here's what each Medicare Supplement plan covers. Remember: all companies offer the same benefits for each plan letter—only price and service differ.

| Benefit | A | B | D | G | K | L | M | N |

|---|---|---|---|---|---|---|---|---|

| Part A coinsurance & hospital | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| Part B coinsurance | 100% | 100% | 100% | 100% | 50% | 75% | 100% | 100%** |

| Blood (first 3 pints) | 100% | 100% | 100% | 100% | 50% | 75% | 100% | 100% |

| Part A hospice coinsurance | 100% | 100% | 100% | 100% | 50% | 75% | 100% | 100% |

| Skilled nursing coinsurance | No | No | 100% | 100% | 50% | 75% | 100% | 100% |

| Part A deductible | No | 100% | 100% | 100% | 50% | 75% | 50% | 100% |

| Part B deductible | No | No | No | No | No | No | No | No |

| Part B excess charges | No | No | No | 100% | No | No | No | No |

| Foreign travel emergency | No | No | 80% | 80% | No | No | 80% | 80% |

| Out-of-pocket limit | N/A | N/A | N/A | N/A | $8,000 | $4,000 | N/A | N/A |

** Plan N pays 100% of Part B coinsurance, except up to $20 copay for office visits and up to $50 copay for ER visits (waived if admitted)

Medicare Supplement Costs

Medicare Supplement premiums vary based on several factors. Understanding how companies price plans helps you find the best value:

Community-Rated (No-Age-Rated)

Everyone pays the same premium regardless of age. Rates increase for everyone at the same time. Fair for older enrollees.

Issue-Age-Rated

Premium based on your age when you first buy the policy. Rate doesn't increase because you get older (only general increases).

Attained-Age-Rated (Most Common)

Premium increases as you get older. Starts lower but increases annually with age. Most Texas insurance companys use this method.

Regardless of the pricing method, premiums will change each year.

- • Age: Premiums generally increase with age (except community-rated plans)

- • Gender: Women often pay less than men (women statistically use less healthcare)

- • ZIP code: Location affects rates based on regional healthcare costs

- • Tobacco use: Smokers may pay 15-30% more

- • Household discount: Some companies offer discounts if both spouses have policies

| Age | Monthly Premium Range |

|---|---|

| 65 | $130-180 |

| 70 | $150-200 |

| 75 | $170-230 |

| 80 | $200-270 |

Rates vary by insurance company, ZIP code, gender, and tobacco use. These are estimates only.

When to Buy: Open Enrollment Period

The BEST time to buy a Medicare Supplement plan is during your Medicare Supplement Open Enrollment Period. This is your guaranteed acceptance period. The insurance company cannot deny you coverage and cannot ask any health questions.

Critical: Don't Miss Your Open Enrollment!

Your Medicare Supplement Open Enrollment Period lasts 6 months, starting the first day of the month you're both 65 or older AND enrolled in Medicare Part B.

During this period, insurance companies MUST sell you any Medigap policy they offer, regardless of your health. They can't charge you more, deny you coverage, or exclude pre-existing conditions. After this period ends, you may be subject to medical underwriting.

What Happens If You Miss Open Enrollment?

After your 6-month open enrollment period ends, insurance companies in most states can:

- • Use medical underwriting (review your health history)

- • Deny you coverage altogether

- • Charge you significantly higher premiums

- • Exclude coverage for pre-existing conditions (for up to 6 months)

Some states have additional guaranteed issue rights. Contact me to discuss your situation if you've missed your open enrollment.

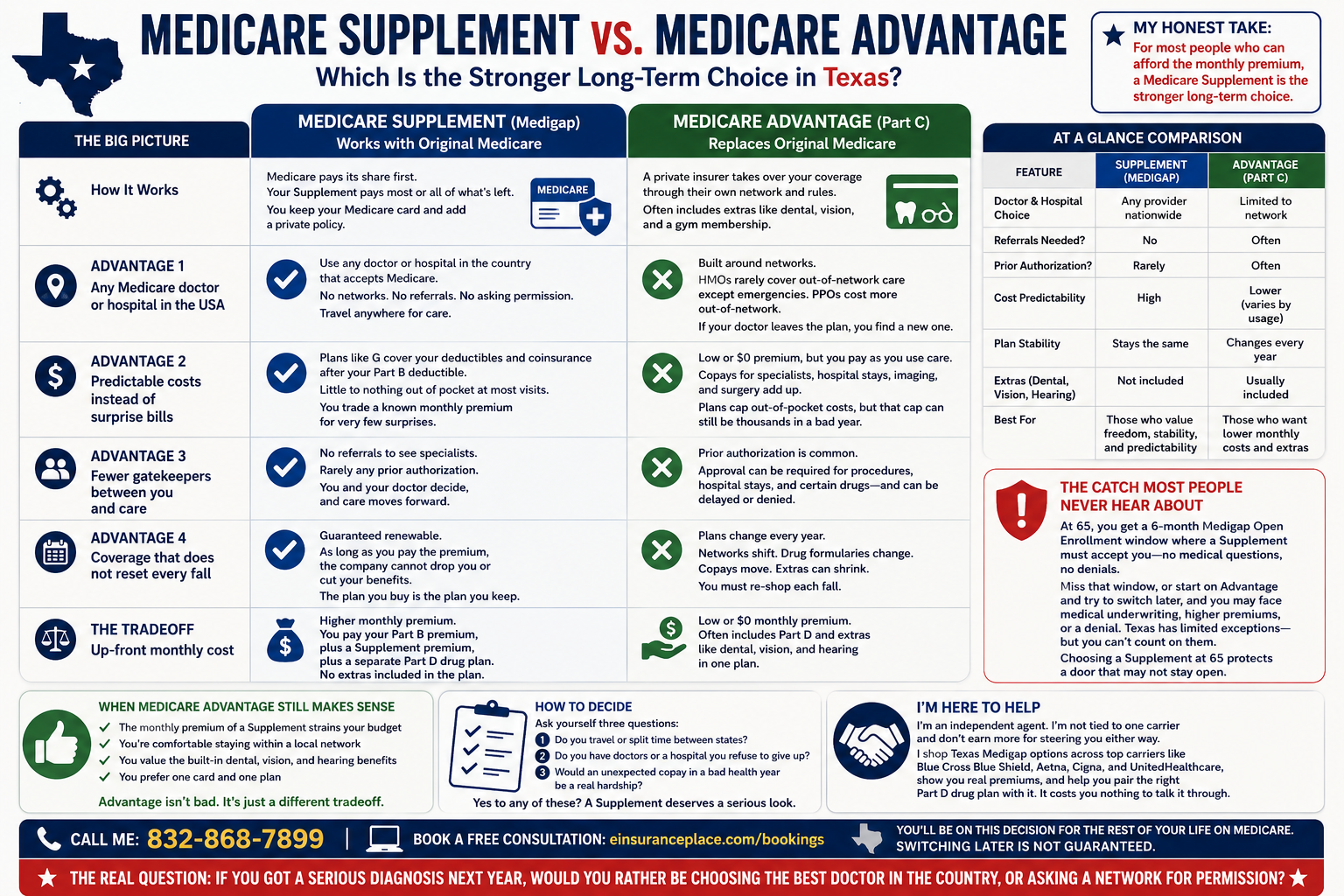

Medicare Supplement vs. Medicare Advantage

Not sure whether to choose Medicare Supplement or Medicare Advantage? Here's a direct comparison:

| Medicare Supplement | Medicare Advantage | |

|---|---|---|

| Medicare Part A & B | Required | Required |

| Original Medicare | Works with Part A & B | Replaces Part A & B |

| Premium | $80–$160 | $0–$167 |

| Prescription Drugs | Part D plan | Included |

| Choose Best Drug Plan? | Yes | No—take what company gives you. |

| Out of Pocket Costs | After Part B deductible, pays 100% | Has Copays and Coinsurance up to $13,300 |

| Maximum Out of Pocket | $0—Pays 100% | $8,250 In-Network, $13,900 for In-Network and Out-Network combined. |

| Prior Authorization | No, No, and No again! | Insurance company and AI decide what treatment you can have—NOT your doctor |

| Guaranteed Renewable? | Yes | No—Plans change every year. Plans are canceled every year. |

| Benefits Medicare doesn't cover? | No | Some, like dental and vision |

| Healthcare expenses | Pays ALL out-of-pocket costs after Medicare pays its share. | Insurance Company Responsible for paying for Healthcare, not Medicare. |

| Choose your doctor and hospital? | Yes—Can use ANY doctor in USA that accepts Medicare. Can use ANY Hospital In USA that accepts Medicare. | NO—Must use insurance company's limited doctor/hospital Network. |

| Specialist referral required? | No | Yes—Most HMOs require specialist referral. |

| Cost Sharing | Change to up to $20 doctor office visit copay $50 emergency room copay (waived if admitted) | $0–$13,900. |

| Deductibles | Annual Part B $283 deductible | Some plans have up to a $1,000 Medical Deductible before the plan pays anything and up to the $615 deductible for Prescription Drugs |

| Covered out of town? | Anywhere in USA, $50,000 out of country | Only in life threatening emergency in USA |

| Expanded benefits | No | OTC, Home Meals after Hospital, transportation |

Choosing an Insurance Company

Since all companies offer the same benefits for each plan letter, your choice comes down to:

- Price - Premiums vary significantly by insurance company for the same coverage

- Financial stability - Choose A.M. Best rated companies

- Customer service - Claims processing, phone support, online tools

- Rate increase history - Some companies raise rates more frequently/aggressively

Who Benefits Most from Medicare Supplement?

Medicare Supplement plans are ideal if you:

- Want complete freedom to see any Medicare-accepting doctor nationwide

- Have specialists you see regularly

- Travel frequently or spend time in multiple states

- Prefer predictable, low out-of-pocket costs

- Want coverage that doesn't change year-to-year

- Don't want to deal with referrals or prior authorization

- Have complex health conditions requiring frequent care

Get Expert Medicare Supplement Help

Choosing the right Medicare Supplement plan and company requires comparing dozens of options. I can help you:

- Determine your 6 month Open Enrollment Period with no health questions asked

- Compare all Medigap plans and explain the differences

- Get quotes from every insurance company in Texas

- Understand pricing methods and rate increase history

- Calculate your total annual costs (premiums + out-of-pocket)

- Apply for coverage during your guaranteed issue period

Compare Medicare Supplement Plans

Let's discuss your healthcare needs and compare Medigap plans from all Texas insurance companys. Free consultation, no obligation. Act during your open enrollment period for guaranteed issue.