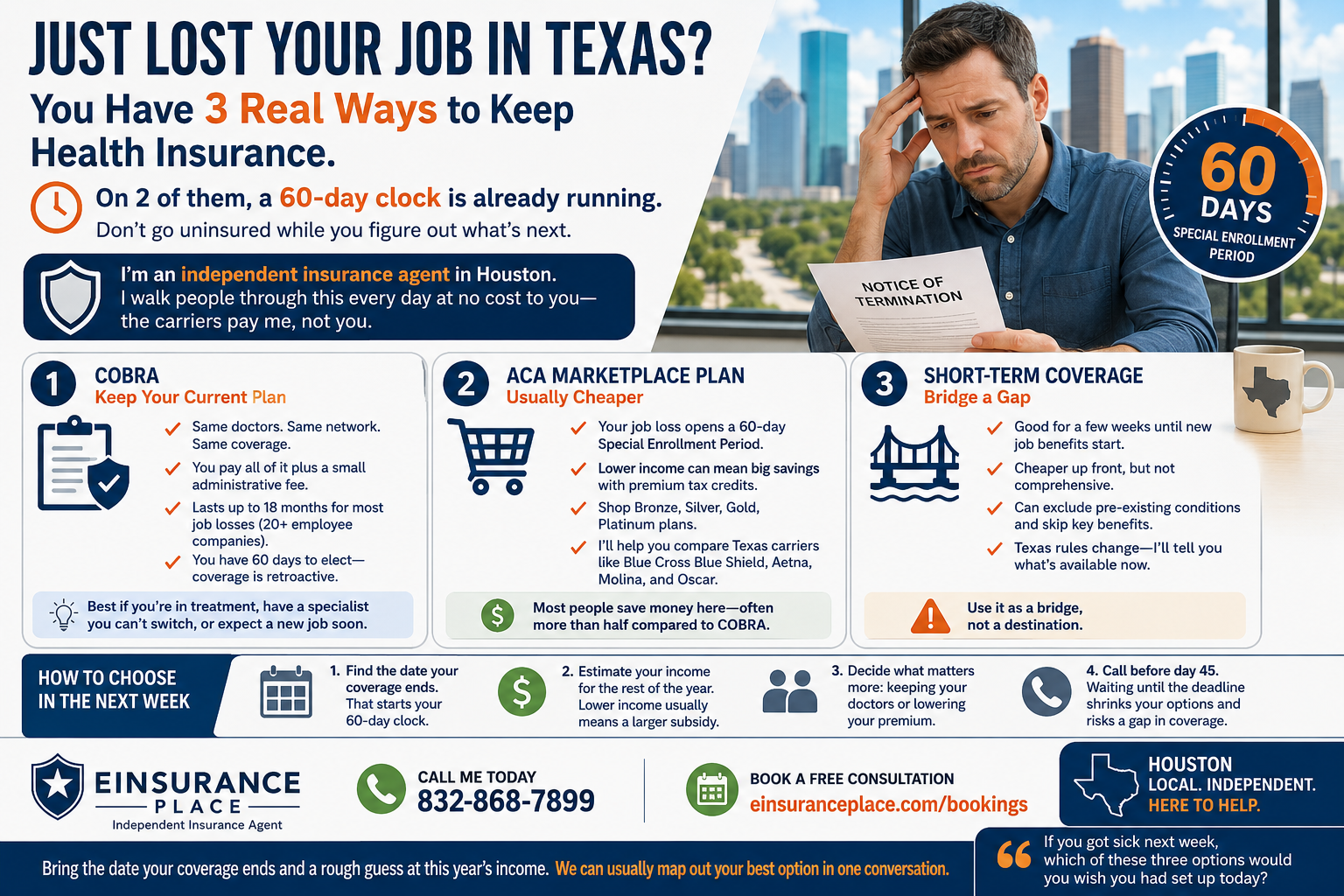

Lost Your Job in Texas? How to Get Health Insurance Fast

If you just lost your job in Texas, you have three real ways to keep health insurance, and on two of them a 60-day clock is already running. You do not have to go uninsured while you figure out what comes next. I am an independent insurance agent in Houston, and walking people through exactly this moment is what I do at no cost to you, because the carriers pay me, not you.

First, know your deadline

Losing job-based coverage opens a 60-day Special Enrollment Period. That is your window to pick a new plan without waiting for the usual fall open enrollment. Miss it, and you may be locked out until the next open enrollment or another qualifying life event.

So before you compare anything, find the exact date your old coverage ends. Every option below runs off that date.

Option 1: COBRA keeps the plan you already have

COBRA lets you continue the exact plan you had at work. Same doctors, same network, same coverage. The catch is the price. Your employer was quietly paying most of your premium, and now you pay all of it plus a small administrative fee.

How long does COBRA last in Texas

For most job losses, federal COBRA runs up to 18 months, and it applies to companies with 20 or more employees. If your employer was smaller than that, federal COBRA may not cover you, but Texas state continuation coverage works in a similar way for many small-group plans.

You have 60 days to elect COBRA after your coverage ends, and it is retroactive to the day you lost it. That means you are not exposed during the decision window, even if you wait a few weeks to sign up.

COBRA makes the most sense when you are in the middle of treatment, have a specialist you cannot switch, or expect a new job with benefits within a month or two.

Option 2: An ACA Marketplace plan is usually cheaper

For most people I talk to, a Marketplace plan ends up costing less than COBRA, sometimes far less. Losing job coverage qualifies you for that same 60-day Special Enrollment Period, and it also opens the door to premium tax credits based on your new, lower income.

Here is the part people miss. While you were employed, your income was probably too high for much of a subsidy. Now that the paycheck stopped, your expected income for the year drops, and the subsidy can climb. I have watched people cut their monthly premium by more than half just by moving from a COBRA quote to a Marketplace plan.

You can shop across Bronze, Silver, Gold, and Platinum tiers, and I can tell you which Texas carriers, including Blue Cross Blue Shield, Aetna, Molina, and Oscar, keep your current doctors in network.

Option 3: Short-term coverage to bridge a gap

If you already have a new job lined up and only need to cover a few weeks before those benefits start, short-term medical can bridge the gap. It is cheaper up front, but it is not comprehensive.

Short-term plans can exclude pre-existing conditions and skip benefits that ACA plans are required to cover. Texas rules on how long these plans can last have shifted in recent years, so I will tell you exactly what is available right now and whether it actually fits your situation. Treat it as a bridge, not a destination.

How to choose in the next week

Find the date your coverage ends. That starts your 60-day clock.

Estimate your income for the rest of the year. Lower income usually means a larger Marketplace subsidy.

Decide whether keeping your exact doctors matters more than your premium. If it does, COBRA buys you time. If not, compare Marketplace plans first.

Call before day 45. Waiting until the deadline shrinks your options and risks a gap in coverage.

What this costs you

Nothing to work with me. I am an independent agent, which means I am not tied to any single insurance company. I shop the whole Texas market, lay out the real numbers side by side, and you pay the same premium you would pay going direct to the carrier.

If a Marketplace plan beats your COBRA quote, I will say so. If COBRA is genuinely your best move, I will tell you that too.

If you just lost your job, call me at 832-868-7899 or book a free consultation at einsuranceplace.com/bookings. Bring the date your coverage ends and a rough guess at this year's income, and we can usually map out your best option in one conversation.

The hardest part of losing a job is rarely the insurance paperwork. It is making a clear decision while everything else feels uncertain. So ask yourself one thing before those 60 days slip past: if you got sick next week, which of these three options would you wish you had set up today?

Larry Fisackerly

Written by Larry Fisackerly with first-hand expertise. AI tools may be used for research and drafting assistance, but all content is reviewed, verified, and published by the author.