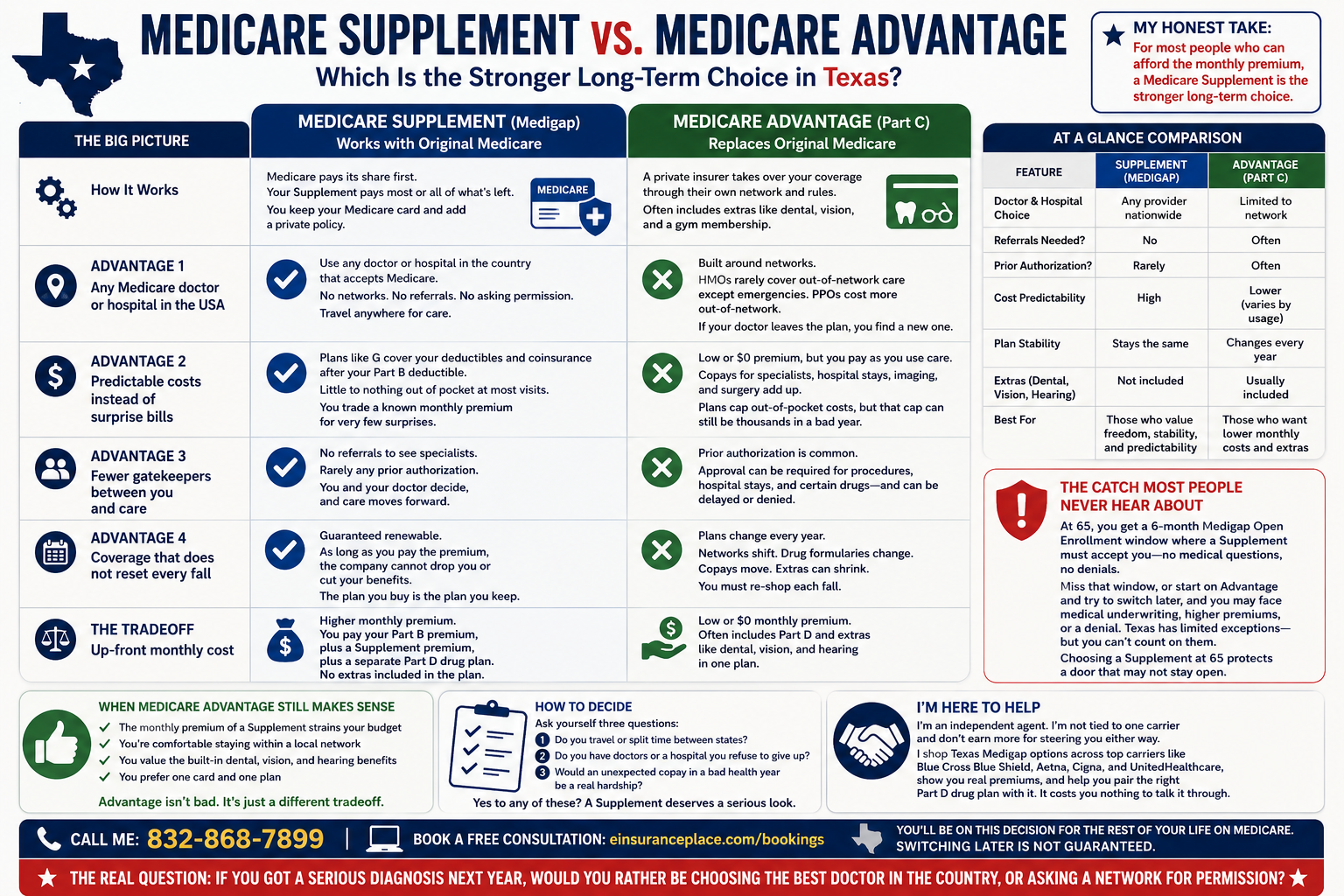

Medicare Supplement vs. Medicare Advantage: Why a Supplement Wins

If you are turning 65 in Texas and deciding between a Medicare Supplement and a Medicare Advantage plan, here is my honest take after years of doing this: for most people who can afford the monthly premium, a Medicare Supplement is the stronger long-term choice. The single biggest reason is freedom. A Medicare Supplement lets you use any doctor or hospital in the country that accepts Medicare, and almost all of them do. No networks, no referrals, no asking permission.

That one difference shapes almost everything else. Let me walk through it.

The core difference in how each plan is built

A Medicare Supplement, also called Medigap, works alongside Original Medicare. Medicare pays its share first, and your Supplement pays most or all of what is left. You keep the government Medicare card, and you add a private policy that fills the gaps.

A Medicare Advantage plan replaces Original Medicare. A private insurer takes over your coverage and runs it through their own network and their own rules. Many of these plans cost zero dollars in monthly premium and add extras like dental, vision, and a gym membership.

Both are legitimate. But they behave very differently the day you actually get sick.

Advantage 1: Any Medicare doctor or hospital in the USA

With a Supplement, if a provider accepts Medicare, you are covered. That includes top hospitals across the country. If you want to travel to MD Anderson in Houston, the Mayo Clinic, or a specialist three states away, you go. You do not need that provider to be in network, because there is no network.

Medicare Advantage plans are built around networks. HMOs keep you inside a defined list of doctors and often will not pay at all for out-of-network care except in an emergency. PPOs give you more room, but you still pay more to step outside the network. If your favorite specialist leaves the plan next year, that is your problem to solve.

For a lot of my clients, that freedom is the whole ballgame.

Advantage 2: Predictable costs instead of surprise bills

A comprehensive Supplement like Plan G covers your Medicare deductibles and coinsurance after you pay the small annual Part B deductible. For most of the year, you hand over your two cards and owe little to nothing at the point of care. You trade a known monthly premium for very few surprises.

Medicare Advantage works the opposite way. The premium is low or zero, but you pay as you use care. Copays for specialists, hospital stays, imaging, and outpatient surgery add up, and they land when you are already sick and least able to shop around. These plans do cap your annual out-of-pocket spending, which Original Medicare alone does not, but that cap can still run into thousands of dollars in a bad year.

Advantage 3: Fewer gatekeepers between you and care

Original Medicare with a Supplement does not require referrals to see a specialist, and it rarely requires prior authorization. You and your doctor decide, and care moves forward.

Medicare Advantage plans lean heavily on prior authorization. The plan can require approval before a procedure, a hospital admission, or certain drugs, and that approval can be delayed or denied. When you are dealing with a serious diagnosis, fighting your own insurance company for permission is the last thing you want to be doing.

Advantage 4: Coverage that does not reset every fall

Medicare Advantage plans change every year. Networks shift, drug formularies change, copays move, and the extra benefits that looked great in the brochure can shrink. You are expected to re-shop your plan each fall to make sure it still fits.

A Supplement is guaranteed renewable. As long as you pay the premium, the company cannot drop you or cut your benefits because your health changed. The plan you buy is the plan you keep.

The one real tradeoff: the monthly premium

I promised honesty, so here it is. A Supplement costs more up front. You pay a monthly premium for the Supplement, you pay your Part B premium, and you buy a separate Part D drug plan, since Medigap does not include prescriptions. Medicare Advantage often bundles all of that into a single low-cost or zero-premium plan with extras attached.

So the real question is not which plan is cheaper this month. It is which plan you would rather have the year something goes seriously wrong. A Supplement asks you to pay a steady, predictable amount while you are healthy in exchange for freedom and stability when you are not. For most people planning to be on Medicare for decades, that trade is worth it.

The catch most people never hear about

Here is the part that changes the decision for a lot of people. When you first enroll at 65, you get a six-month Medigap Open Enrollment window where a Supplement must accept you regardless of your health. No medical questions, no denials.

Wait past that window, or start on Medicare Advantage and try to switch to a Supplement later, and in most cases the insurer can put you through medical underwriting. If your health has declined, they can charge you more or turn you down entirely. Texas has limited exceptions, but you cannot count on them.

That is why choosing a Supplement at 65, while you are healthy and guaranteed acceptance, protects a door that may not stay open. It is a lot easier to start with a Supplement than to qualify for one at 72.

When Medicare Advantage still makes sense

Advantage is not a bad product, and I enroll people in it every year when it fits. It can be the right call if the monthly premium of a Supplement genuinely strains your budget, if you are comfortable staying within a local network, or if the built-in dental, vision, and hearing benefits matter more to you than nationwide freedom. Some people simply prefer one card and one plan.

The point is to choose with your eyes open, not to get pulled in by a zero-dollar premium without understanding what you trade for it.

How to decide

Start with three questions. Do you travel or split time between states? Do you have doctors or a hospital you refuse to give up? Would an unexpected copay in a bad health year be a real hardship? If you answered yes to any of them, a Supplement deserves a serious look.

I am an independent agent, which means I am not tied to one carrier and I do not earn more for steering you to Advantage or to a Supplement. I shop Texas Medigap options across carriers like Blue Cross Blue Shield, Aetna, Cigna, and UnitedHealthcare, show you the real premiums, and help you pair the right Part D drug plan with it. It costs you nothing to talk it through.

Call me at 832-868-7899 or book a free consultation at einsuranceplace.com/bookings before your enrollment window closes.

You will be on this decision for the rest of your life on Medicare, and switching later is not guaranteed. So ask yourself the real question: if you got a serious diagnosis next year, would you rather be choosing the best doctor in the country, or asking a network for permission?

Larry Fisackerly

Written by Larry Fisackerly with first-hand expertise. AI tools may be used for research and drafting assistance, but all content is reviewed, verified, and published by the author.